Can I buy a house with my salary? How do you actually know how much house you can afford?

How would you like to own your first home?

Imagine, no longer having to pay rent. You own your living space, so you can do whatever it is you please.

Home ownership is a wonderful thing, but it can also be stressful. So many things can go wrong. The last thing you need is an expensive repair you didn’t plan for.

Luckily for you, I’m going to show you how much house you can afford to ease the transition. It doesn’t matter if you make $50k per year or a $100k salary. The principles for buying your first home are the same.

This article may contain affiliate links which pays a commission and supports this blog. Thank you for your support!

Can I buy a house with my salary?

Understanding if you can buy a house on your salary takes one skill, budgeting. Someone who is an expert budgeter can plan their future home expenses.

Ultimately, the bank will tell you how much money you are allowed to borrow. However, the bank will often allow you to borrow more money than you can financially handle. Lenders will determine your loan eligibility by looking at:

- Your Debt to Income ratio. Debt to Income ratio is the amount of debt your in, home loan included, compared to your income.

- Consistent income. Showing a history of earning income provides the bank with confidence you’ll continue to be able to afford your loan.

- History of paying bills on time. Are you reliable enough to pay back the mortgage?

- Your down payment and cash on hand. The bank wants to know if they are taking the full risk or do you have equity involved. Do you have enough cash to cover expenses when moving into your home.

Credit score plays a large part in the interest rate you’ll be charged. A high credit score means you’re less risky to loan money to, earning you a lower rate.

To be a successful first-time home buyer, you need to determine for yourself how much house you can buy. Then, tell your mortgage broker and realtor what your expected monthly payment should be.

Here is the step-by-step instructions for determining a monthly mortgage payment that you can afford.

Step #1 – Determine your take home income

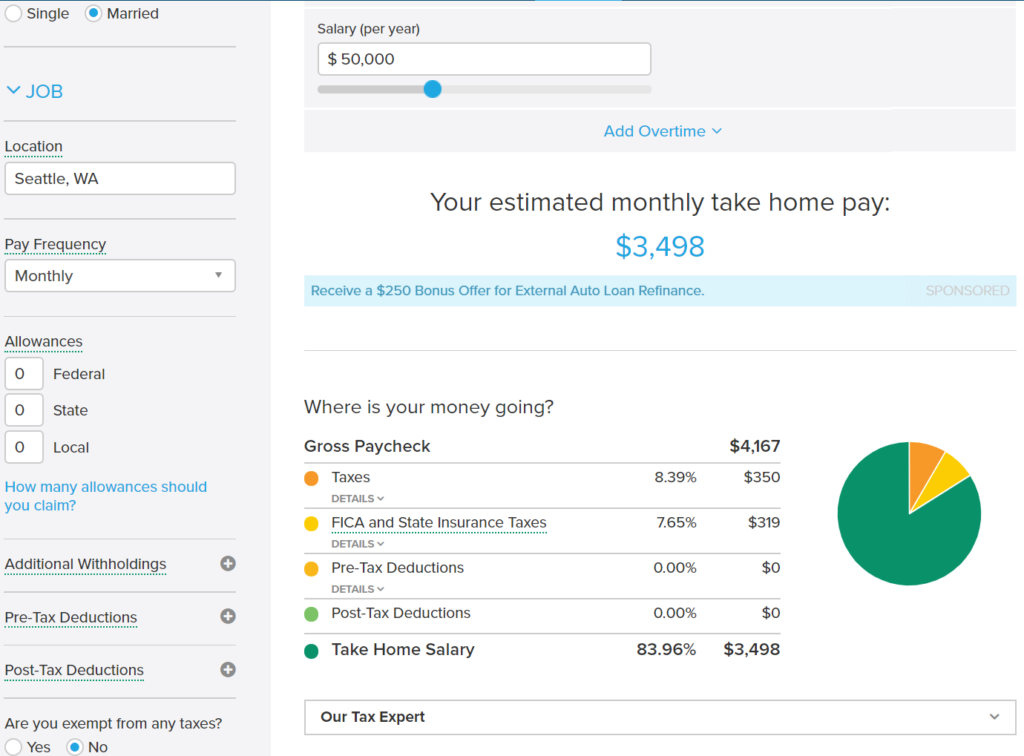

The easiest way to determine your take home pay is to check your paystub. Otherwise, you can use a free paycheck calculator to estimate your household income.

Your take home pay is determined based on a number of factors. Obviously, the largest factor is what your gross annual salary is. Your net income is determined based on factors such as marital status, allowances (Federal, State, and Local), pre and post tax deductions.

Assuming you’re married and aren’t claiming additional withholding’s (e.g. claim zero allowances, pre and post tax deductions), a 50k salary is $3,498 per month in take home pay.

Salary (per year)

Salary is your agreed upon yearly wage, before taxes are taken out. If you don’t know your salary, your HR department can tell you.

Don’t count any overtime or bonuses when determining your take home pay for purchasing a home. You should only consider consistent income sources to see how much home you can afford.

Pay frequency

Enter in how frequently you’re paid. The SmartAsset paycheck calculator has the following options:

- Daily – Paid once per day.

- Weekly – Paid once per week.

- Bi-Weekly – Paid ever other week. There are 26 pay periods in one year.

- Semi-Monthly – Paid twice per month. Usually paid on the 15th and the last day of the month.

- Monthly – Paid once per month.

- Quarterly – Paid four times per year (once every three months).

- Semi-Annually – Paid once every six months or twice per year.

- Annually – Paid once every year.

Allowances

Your allowances are what you filed on your W-4 when you accepted your job or last updated. You can request a copy or get your W-4 updated through your HR Department. Updating your W-4 will change how much tax is withheld from your paycheck.

Pre-Tax Deductions

Pre-Tax deductions are money that is removed from your gross salary before taxes take affect. You can use pre-tax deductions to save money or deffer taxes on your income.

For example, maybe you want to contribute $300 per month to your 401k. Your take home pay is only reduced by $264, meaning you can earn interest by investing the $36 difference. However, taxes are paid once the money is withdrawn during retirement.

A list of available pre-tax deductions include:

- Medical Insurance

- Dental Coverage

- Vision Insurance

- 401k Contributions

- Long Term Disability Insurance

- Life Insurance

- Commuter Plan

- FSA

- HSA

Post-Tax Deductions

Post-Tax deductions take place after taxes have been accounted for. Your employer may offer specific post-tax deductions that may be applicable to your situation.

Click to Tweet! Please Share!Click To TweetStep #2 – Determine your monthly expenses

Next, create a list of monthly expenses. What is it you spend your money on regularly? If you already have a household budget, now would be a good time for you to review it. Otherwise, now is the time to create a budget that you can follow.

Dave Ramsey has recommended budget percentages which can act as your guideline. You should follow these percentages as a starting point.

You should also make sure your emergency fund is fully funded before purchasing a home. An emergency fund will help protect your family from any large hidden expenses that might occur.

The goal is to create a budget that you can follow in your current situation. Next, we will find out how these expenses will change when you move into your home.

Click to Tweet! Please Share!Click To TweetStep #3 – What are the home ownership costs?

Home ownership is different than renting. When you’re renting, sometimes you take for granted the services being provided to you when you pay your rent. You will now be expected to pay for all home repairs and maintenance costs.

Transitioning into a new home can be difficult. Make every effort to catch potential problems before you purchase a home. However, sometimes problems come up after purchasing a home.

The best defense you have is being prepared financially.

Cost of home maintenance?

According to Fool.com, you should expect to pay between 1 and 4 percent of your home’s value in repairs each year. Therefore, for every $100,000 on the purchase price, expect to pay between $1,000 and $4,000.

Alternatively, you can budget $1 for every square footage of your home. Therefore, if you’re home’s square footage is 1,500 square feet, budget $1,500 per year. Budgeting based on square footage doesn’t account for home location, such as high humidity areas.

Both methods above are a simple rule of thumb.

Keep in mind, you will also need to budget for major repairs. Eventually, the roof, A/C, and hot water tank will need replacing. You should include extra money in your budget and prepare for such events.

What will your utilities be at your new home?

Moving to a new area can affect your utilities. You need to estimate what your utility expenses will be when you move and incorporate it into your budget.

For example, the town I live in has irrigation water, but the next town over waters their lawns with house water. Your water bill would be significantly higher by living one town over.

Some homes are less insulated and may require more energy consumption. Call your local utilities and they can provide you with estimated cost for a specific property.

However, keep in mind the estimated cost will be what the current owners are paying. You never know if the current owner waters their lawn all day or leaves the lights on. Regardless, these numbers can be used to help you plan your budget.

What home appliances or items will you need to purchase?

Most people are so overwhelmed with the moving process, they completely forget about home appliances or required home maintenance items.

Most likely, you will need to provide your own refrigerator, washer, and dryer. You may also need yard tools, such as a lawn mower and edger.

Click to Tweet! Please Share!Click To TweetStep #4 – How much house can you afford?

Dave Ramsey recommends spending no more than 25 percent of your income on a mortgage payment. Alternatively, the 28/36 rule says you should spend no more than 28 percent of your income on a mortgage payment and no more than 36 percent on total debt.

That being said, 25 percent is a huge amount of your income. Personally, I recommend spending as little of your income on your first home as possible. You can always purchase a second home later down the road when you’re ready to expand.

Remember, the more money you borrow from the bank, the more you’re spending on interest payments. Consider buying low and building some equity before jumping to a higher priced home.

How much money is left in your budget for a mortgage?

In the previous steps, you came up with your total income, your current expenses, and have a rough estimate of what your expenses will be in your new home, except the mortgage.

For example, someone earning $3,500 in take home pay might have the following monthly budget planned for their new home:

- Investing and Savings goals – $600

- Housing expenses – $350

- Utilities – $420

- Food – $450

- Clothing – $70

- Transportation – $350

- Medical Expenses – $75

- Personal Spending – $100

Note the numbers are just for an example. You will have to come up with what’s realistic for your family.

Therefore, total expenses are $2,415. Subtracting expenses from take home pay, leaves you with $1,085 per month to pay your mortgage.

Per this example, you could afford a monthly mortgage payment of $1,085. However, $1,085 is 31 percent of your total income and isn’t recommended. You may want to cut down your payment to 25 percent of your income or $875 per month and save the difference.

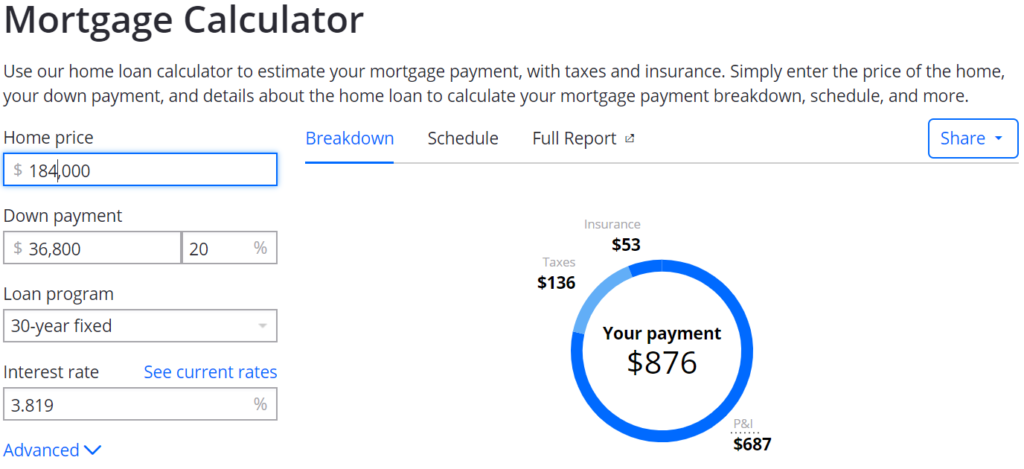

Determine how much house you can afford

Using Zillow’s mortgage calculator, we can see how much house you can afford. For this example, we want our mortgage payment to be around $875 per month.

The mortgage calculator allows you to enter in loan terms until you reach your desired payment. You’ll want to contact your bank to see what current interest rates are for your estimate.

I highly recommend you pay 20 percent down to avoid private mortgage insurance. Private mortgage insurance is extra money you pay if you don’t have the luxury of having a down payment. The bank sees you as a higher risk and will require you to pay the extra money, so the bank doesn’t lose money if you default.

How much house can I buy with my salary? Ballpark estimate.

Here is a table if you want a ballpark estimate based on 25 percent of your annual income. The best thing you can do is go through the steps and determine affordability based on your situation. However, if you’re curious, this table provides an absolute maximum you should pay for your home.

This table assumes a interest rate between 2.8-3.9 percent, you’re paid once per month, and a down payment of 20 percent.

| Salary | 15 year fixed | 30 year fixed |

|---|---|---|

| $50,000 | $154,000 | $218,000 |

| $60,000 | $188,000 | $271,000 |

| $70,000 | $222,000 | $320,000 |

| $80,000 | $258,000 | $370,000 |

Summary: Can I buy a house with my salary?

As you can see, there is a lot that goes into determining if you can afford a house. Budgeting will be the best thing you can do to prepare and determine your price range. The goal is to find a monthly mortgage payment that you’re satisfied with and works for your situation.

Don’t be in a rush to purchase an expensive home. You’ll pay less interest by buying a lower priced home and working your way up.

The first step is to find your monthly take home income. You can use a paycheck calculator if you don’t know what your monthly take home pay is.

Next, you’ll want to create a budget for your current situation that you could live on. You’ll want to estimate the expenses for owning a home and determine what you’ll need to purchase.

How do the new expenses affect your current budget? How much money remains for a mortgage payment?

Finally, use a mortgage calculator to find your maximum home price. Let your lender and realtor know your maximum price point and stick to it. Realtors may try and show you houses above your price point, so don’t be afraid to let them know you can’t afford it.

TightFist Finance

John is the founder of TightFist Finance and an expert in the field of personal finance. John has studied personal finance for over 10 years and has used his knowledge to pay down debt, grow his investment portfolio, and launch a financial based business. He is committed to sharing content related to personal finance based on his experience in his career, investing, and path towards reaching financial independence.