Did you know the age you should retire doesn’t have to be 65? With the right retirement planning you could retire early without relying on social security.

Unfortunately, for most Americans the safe retirement age is rapidly becoming 70!

Do you want to work until 70 to retire?

I didn’t think so. Luckily for you, today I’m showing you what age should you retire and how to retire early, with enough money.

This post may contain affiliate links which pays a commission and supports this blog. Thank you for your support!

Retirement is not an age, but a number

We need to redefine what it means to retire. Age has nothing to do with retirement unless you’re looking to collect social security benefits. Retirement should be more focused on money saved rather than age.

Imagine being 30 years old and having $10 million in investments. Don’t you think you could make $10,000,000 last until you’re 85? Most people won’t even see that much money!

Now, I know $10 million is a pipe dream for most people. What’s really important is finding a dollar amount that provides you with enough income for retirement, regardless of your age.

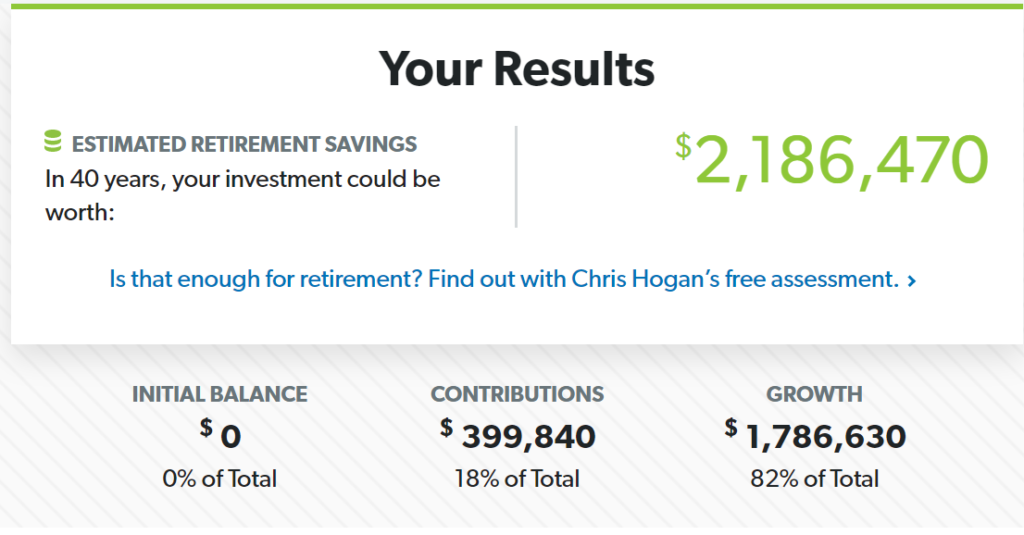

People save and spend money at different rates. Consider a CEO who earns $200,000 but only invests $10,000. Your CEO is blowing $190,000 a year on luxuries and is no better off for retirement than a $40,000 per year earner who invests $10,000.

Both investors would have nearly $2,200,000 investing $10k per year over 40 years. The only difference is the $40k per year earner used their money more efficiently.

To estimate the $2.2M, we used the Dave Ramsey investment and retirement calculator at an assumed 7% return on investment.

So when can you retire? You need to figure out your desired yearly income and your savings rate to know for sure.

Click to Tweet. Please share!Click To TweetHow much money should you have saved for retirement?

So you’ve grasped that retirement is a number and not an age. Next, you need to know about the 4 percent withdrawal rule for stock and bond investments.

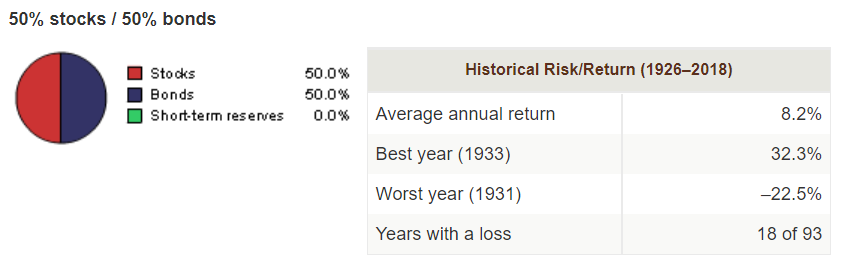

Simply put, you can withdraw 4% of a 50/50 stock/bond portfolio on a yearly basis and almost certainly not run out of money for 30 years. This means that 4% is a sustainable withdrawal rate for individuals in retirement.

Why does this work? Your investments continue to grow as you withdraw a small portion of your portfolio.

According to Vanguard Model Portfolio Analysis, a 50/50 stock and bond portfolio has an average yearly return of 8.2%.

So you’re withdrawing 4%, but gaining 4.2% in annual returns. Personally, I model my own retirement using a 3% withdrawal.

Assuming you keep your money in 100% stocks, Vanguard historical annual returns are 10.1%. Many people often maintain a 100% stock portfolio with a 3-4% withdrawal in retirement.

Related:

But what about stock crashes?

Yep, stock market crashes do happen and you should be ok withdrawing only 3-4%. You will probably end up selling a few extra shares during a crash. However, if planned accordingly, you can withdraw less money during a stock market crash.

Stock market crashes are generally short term and should be expected. Let’s look at the stock market crash of 2008.

As you can see from Barchart’s graph of Dow Jones, the stock market took a hit in 2008. Five years later in 2013, the stock market had made a full recovery.

So how much money do I need invested to retire?

People tend to overthink retirement needs. You should plan on having a minimum of 25 times your annual expenses invested for retirement. 25x annual expenses corresponds to a 4% withdrawal rate.

Not sure what your annual expenses are? You may need to start a budget.

Most people would be comfortable retiring on their current income. If you earn $40,000 per year then you would need $1,000,000 invested [=$40,000 / 0.04 *OR* $40,000 x 25] to maintain your current lifestyle at 4% withdrawal.

Here’s a table that summarizes how much you should have invested to meet your desired income in retirement.

| Desired Retirement Income | Required Investments ($) at 3% Withdrawal Rate | Required Investments ($) at 4% Withdrawal Rate |

|---|---|---|

| $10,000 | 333,333 | 250,000 |

| $20,000 | 666,666 | 500,000 |

| $30,000 | 1,000,000 | 750,000 |

| $40,000 | 1,333,333 | 1,000,000 |

| $50,000 | 1,666,666 | 1,250,000 |

| $60,000 | 2,000,000 | 1,500,000 |

| $70,000 | 2,333,333 | 1,750,000 |

| $80,000 | 2,666,666 | 2,000,000 |

Pre-tax vs. post-tax investing

So I’m sure you’ve probably heard a lot about pre and post-tax retirement planning. Which retirement plan works best for you?

Let’s take a look at the difference between pre-tax and post-tax retirement and how it aligns with your retirement goals.

Pre-tax 401k contributions

The main benefit to pre-tax 401k contributions is tax saving. You invest your money without paying taxes, which helps your money grow faster. Taxes are paid when you withdraw money and are paid according to your tax bracket.

Unfortunately, you cannot withdraw until you are 59.5 years old. Withdrawing early will result in paying a 10% early withdrawal penalty.

Pre-tax 401k contributions are limited by the IRS. In 2020, the maximum you can contribute to a pre-tax 401k retirement account is $19,500.

Most companies offer a 401k match, where they will match your contributions up to a certain percentage of your income. Always contribute enough to receive the free money!

Post-tax investments

Money invested is already taxed, so taxes are only due on any capital gains (growth). You can withdraw money at any time, which allows you to retire, whenever. Many parents use post-tax investments to help pay for their children’s college education.

Planning your retirement

One of the biggest mistakes people make is not planning their retirement. Everyone is so focused on retirement age that they forget to plan retirement by the numbers.

Let’s imagine that you’re a young engineer, age 25, who earns $70,000 per year. You haven’t planned your retirement, but Dave Ramsey suggested you invest 15% of your income into pre-tax 401k. Your company offers a generous 6 percent 401k match.

21% of $70,000 is $14,700 per year or $1,225 per month. Assuming you go by the “Retire at 67” model, you would retire with $3.7 million!

What are you going to do with that much money at 67? That’s a whopping salary of $148,000 per year!

Personally, I like to contribute approximately 10-15% of my income into a 401K. The remainder of my income after expenses goes into an after tax Vanguard account. As I get pay raises, both my pre and after tax contributions grow.

Utilizing both pre and after tax investment accounts allows you to retire early, until you are eligible to withdraw from your 401k.

Many high income earners reach their 50s and find out they can’t retire early because they didn’t invest in after tax accounts. They have no money set aside to carry them until they can withdraw from a 401k.

Low income earners may want to utilize pre-tax retirement accounts to maximize dollars invested. It’s always a good idea to have an after tax account to put unspent money that isn’t set aside for emergencies.

Click to Tweet. Please share!Click To TweetHow do I retire early?

Retirement is a numbers game, it’s not determined by age. I’ve known people who have retired at 30 by investing diligently and 74 year olds who are still working.

Early retirement is possible if you can stop spending money, grow your income, and invest the difference. It’s that simple.

Stop spending money and increase savings rate

The things you buy are keeping you broke and preventing early retirement. Sure, it’s fun to shop deals on Amazon, but frequent small purchases add up.

Cutting expenses will only take you so far. Someone who earns $3,000 per month and cuts $300 off their grocery bill can invest an extra $3,600 per year. However, getting a $12,000 pay raise allows for you to invest an extra $12k every year.

Regular investing

As FourPillarFreedom pointed out, the two factors that influence how fast you can save $1,000,000 are the amount of cash you invest and investment return.

If you want to save $1,000,000 faster, you need to find a high return or increase your contributions. For most people, increasing your contributions is the way to go.

How do I pay for healthcare in retirement?

One of the most common questions or concerns individuals have is paying for healthcare in retirement. I understand that health care isn’t the cheapest in the United States, but there are options.

To start planning retirement healthcare, go to healthcare.gov and click on “get coverage.” Select your state and then select “visit your state marketplace.”

You’ll be directed to your state’s healthcare website. For Washington, I selected browse plans which had my input information about my family. Information includes your birth date, household income, number of people covered, etc.

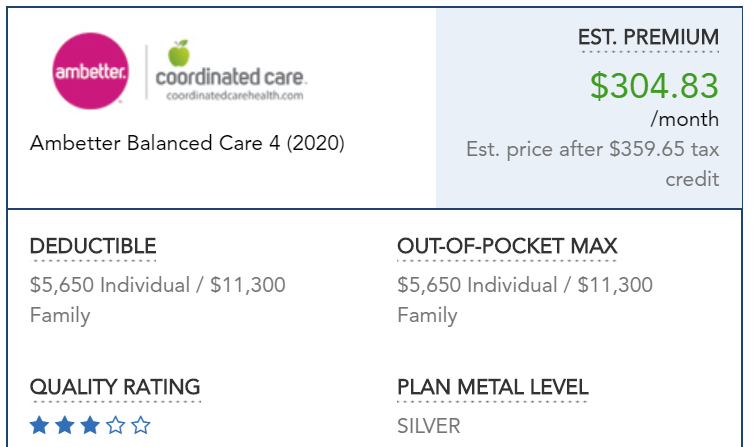

One of the cheapest plans had a monthly premium of $359.65 with a high deductible of $5,650 for an individual or $11,300 for a family.

So yes, healthcare isn’t the cheapest, but it is something that could be included in your budget and retirement planning.

What age can you collect social security?

The earliest you can start collecting social security is 62, but you only get 75% of the benefit. You can collect full benefit from social security once you hit 66. Applications for social security are accepted once you turn 61 years and 9 months.

Summary: What age should you retire?

Hopefully, this article has helped you understand that retirement is not an age, but a number. Yes, for most people it’s an age because they aren’t saving enough money for retirement.

For retirement, you need to have 25x your estimated expenses in retirement. This assumes that you will be withdrawing four percent of your portfolio consisting of 50 percent stocks and 50 percent bonds.

You can choose to have less bonds and more stocks, but your portfolio may be more volatile. A volatile portfolio is more susceptible to stock crashes, which should be expected. Overall, the stock market has consistently risen over time.

Planning your path to retirement is important. High income earners may end up with too much in pre-tax 401k accounts while low income earners may want to increase pre-tax savings for tax breaks. Use a retirement calculator to help plan your retirement funds.

If you want to retire early, you need to cut your expenses, grow your income, and invest the rest.

Healthcare is expensive and should be planned into your retirement savings. Shop for healthcare on healthcare.gov to estimate your plans expenses.

Social security can be collected as early as 62, but you’ll receive full benefit at age 66. Social security should be planned as an added bonus, and not relied on for retirement.

TightFist Finance

John is the founder of TightFist Finance and an expert in the field of personal finance. John has studied personal finance for over 10 years and has used his knowledge to pay down debt, grow his investment portfolio, and launch a financial based business. He is committed to sharing content related to personal finance based on his experience in his career, investing, and path towards reaching financial independence.