Paying off debt can feel like an impossible task, but it doesn’t have to be.

Families across the U.S. are becoming more in debt and fighting over money issues.

Taking out a loan to pay for college, a new car, home, or other big expense now feels burdensome as you try and pay off your debt.

With taking on more debt, it can feel nearly impossible to get ahead in life or even just paying the bills.

However, with a little hard work and this strategy, you and your family can be debt free.

Today’s article is all about paying off your debt quickly and developing a plan to pay off your debt in full.

This post may contain affiliate links which pay a commission and supports this blog. Thank you for your support!

The ultimate guide to paying off debt

Breaking down debt: The simple equation with big results

To truly make progress on your debt, you need to understand what debt is and how it’s created. Once you understand the basic premise of debt you can make huge leaps towards paying off debt.

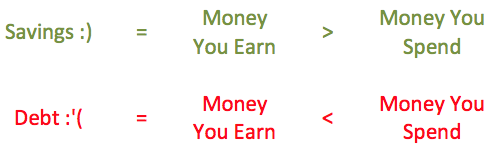

Debt is simply the result of negative cash flow. Cash flow is just a fancy word for evaluating how much cash enters your bank account versus how much leaves.

When you start spending more money than you’re earning, you create debt. The flip side is when you start saving more money than you’re earning, you build wealth.

So our goal is to change our cash flow so that we earn more money than we have exiting our bank accounts each month.

Related:

- Here’s how to budget LIKE THE MILLIONAIRES do!

- Ready to go on a vacation but have no money? Here’s how to plan your next trip, CHEAP!

- Here’s the exact strategy we used to PAY OFF 40% of our mortgage in 2 YEARS!

Why is cash flow so important?

As you begin to pay off your debts, one by one, you’ll start to have fewer expenses. With fewer expenses comes more cash to pay off debt.

This is the simple concept of leverage.

Why is leverage so important?

Well for someone in debt, leveraging their extra cash will help them pay off debt faster.

For the wealthy, leveraging cash is how they become millionaires and even billionaires.

A wealthy person knows they can get a loan from a bank and purchase an apartment complex. Depending on the situation, the wealthy person may not have to put any money towards a downpayment.

If that apartment complex has 18 units with a rent of $1,000, the owner now generates $18,000 in monthly income.

Now a smart investor usually doesn’t pocket all that money, they pay off the loan and save for emergencies. If done right, the wealthy person should be generating more cash than the mortgage or other expenses.

Our wealthy person is building equity by paying off the loan with rental income. The apartment may appreciate in value, meaning they could sell it and earn money as the apartment value rises. Once the mortgage is paid off, the wealthy person now has a steady income of $18,000 per month.

Building a debt smashing budget

The first step in paying off your debt should begin with building a monthly budget.

With proper budgeting, you can go into a new month and already know how much money you’ll save.

When you know how much money you’ll save, you know how much money can be paid towards debt!

Budgeting will allow you to see what areas of your life need improvement. For myself, eating out is a huge weakness and my budget helps keep me accountable.

No budget is ever perfect the first time. You will most likely need to update your budget regularly depending on how the month went.

For example, my wife and I discuss our budget every month making minor adjustments as needed.

So here are a few steps to help you start building a debt crushing budget!

Related:

- You need to follow these BUDGET TIPS for a DEBT FREE LIFE.

- Are you asking yourself these 10 IMPORTANT money saving questions?

- Will your child grow up in debt or become wealthy? You can help them with these easy tips.

Identify your monthly net income

How much money does your family bring home every month?

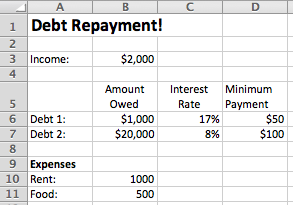

When building a debt-busting budget, it’s best to identify your lowest possible income for the month. Meaning if you get paid anywhere from $2,000 to $2,500 each month, write down the $2,000.

Budgeting on your lowest possible income means your budget will always add up at the end of the month. You can’t plan your budget expecting to bring home $2,400, but you had a bad month and were $200 short.

I would much rather estimate my income low and have extra money to save each month than estimate high and struggle to pay the bills.

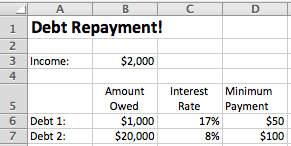

Identify your debts, interest rates, and minimum payments

Without counting your mortgage, what debts do you owe and what are the interest rates and minimum payments on each?

This should be fairly self-explanatory, but think of what credit cards, car loans, student loans, etc, you might have.

For example, you might have a credit card balance of $1,000 at 17% interest and a minimum payment of $50 per month. You could also have a $20,000 car loan at 8% interest with a minimum monthly payment of $100.

Identify your monthly expenses

So you’ve identified your debts, but what about all the other expenses of your life?

Now you should write down all your monthly expenses such as groceries, tv, rent/mortgage, utilities, insurance, etc. How much are you currently spending on each of these items?

Assign your expenses and debts into categories and subcategories

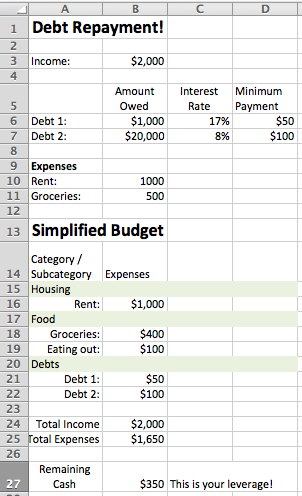

Now we need to start organizing your budget by creating different categories and subcategories.

Categories are broad terms, such as food. Food can be divided into subcategories, groceries and restaurants.

You’ll want to build categories and subcategories for all your identified monthly expenses. Remember, think of categories like utilities and subcategories like electric and water.

Don’t forget to identify things you should budget for even if you don’t pay on a regular basis.

You should be budgeting for emergencies and have a subcategory for items such as auto-repair. You’ll need to have money set aside for when life doesn’t go as planned, such as a broken down car.

Other examples would include saving for retirement (if done after tax), yearly membership fees, tire replacement, etc.

Start assigning rough dollar values to each subcategory. This amount is what you plan to budget for each month for each subcategory.

You should try and choose a reasonable dollar amount that you can live off of, but not be too extravagant. For example, you might say that you will spend $400 per month on groceries.

For your debts, just do the minimum payment while estimating your other monthly expenses.

Check your income vs expenses

The first step after estimating your monthly expenses is to see how much money remains?

In the previous step, you estimated a rough budget by identifying what your monthly expenses cost you each month. How do your expenses compare to your income?

So in the last step, if you estimated your monthly expenses as needing $1,650 each month and you earn $2,000, $350 remains.

This money that remains is your leverage.

You can now use that $350 per month to pay down debt. I’ll talk more later on debt repayment strategies that will work best for you.

Ideally, your income is greater than your expenses. However, that isn’t always the case. If you’re spending more than you earn you can either reduce your expenses or earn more money.

Share this article on Twitter!Click To TweetReduce expenses as needed

You can increase your leverage (money saved every month) by reducing your expenses.

This is one of the least favorite parts of any adult when it comes to budgeting, but also one of the most important parts.

Reducing your expenses is all about setting limitations that you expect yourself to follow. No one is going to keep you accountable if you’ve maxed out your eating out budget and then buy a pizza.

Should you overspend in any subcategory, you’ll need to find out how to cover the difference. Unfortunately, that normally comes from your extra monthly savings which means you aren’t paying off debt as fast.

What expenses can you reduce in your budget that might be a bit too high? Did you give yourself $100 for free spending, but could do with $50?

The more money you can save, the more money you can use toward debt repayment!

Read the ultimate guide to budgeting for tips on building an effective budget

This article is only a small portion of what it takes to build an effective budget. If you’re serious about paying off debt then you need a strong budget!

That’s why I’ve written the ultimate guide to budgeting and created a free course to get your budgets off to a good start.

Both the article and the free course are packed with the information you need to build a budget and get out of debt.

Evaluating your household income

Remember, there are two ways to increase the money you save each month (leverage for debt repayment). You can either reduce your expenses or increase your income.

For some families in debt, they may be surprised to find out their income is not adequate.

So how do you determine if your income is adequate enough to repay debt and start building wealth? You start by asking yourself if you earn money enough to be considered average.

Do you earn enough to be considered average?

The first concept for evaluating your household income is ensuring that you earn at least an average income for your city.

Why is it important to earn an average income?

Simply stated, your city has a local economy that would not survive if it couldn’t support the “average” person.

If the average household income for your city was $40,000, but apples cost $10 each, no one could afford to live because expenses are too high for the average person to live.

Earning less than average isn’t normally considered a good thing. When did you ever feel good in school about getting a D on a test when the class average was a C+?

People who earn less than average might earn a salary considered to be “livable” in some cases, but you won’t build wealth on a “livable” salary. Usually, a livable salary means you’re living paycheck-to-paycheck.

Your goal, should be to earn at least an average income, if not greater than average.

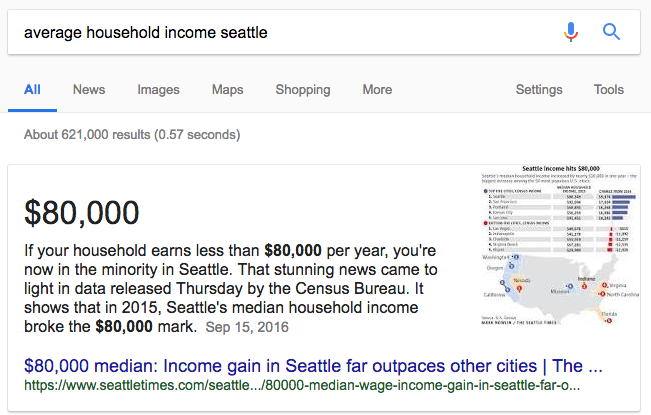

So how do you determine what the average household income is? Start by doing a quick google search for “your city” + “average household income”

How does your income compare?

What is the cost of living where you live?

There is a very important financial aspect to your city that not a lot of people seem to understand, but it’s very important.

Each city has their own local economy, which means it can be more expensive to live in one city than the next. This is measured by the cost of living index.

Every city has a cost of living index and it’s a powerful tool to help you decide whether or not living in a city is worth it financially.

A city with a cost of living index of 100 is considered average, not expensive but not a cheap place to live. Over 100 is considered an expensive place to live and under 100 is considered inexpensive.

It is most ideal to live in a city with a cost of living index under 100.

Most larger cities, such as Seattle or New York would be considered expensive to live in. Usually, these cities are not a good place to live in if you are trying to get ahead in life.

Why do people live in expensive cities? A lot of people love the city life, but they make a financial sacrifice to live in a big city.

Personally, I would never be caught living in a large city, but I would rather have money and I don’t want to be surrounded by that many people.

Debt repayment strategies

There are many different strategies you’ll find online about paying off debt quickly.

So which one will work best for you?

There are only two debt repayment strategies that are worth your time, the debt snowball method and the high-interest payment method.

Both strategies have their strengths, but first, should you pay off your debt or save for emergencies first?

Should you pay off debt or save for emergencies first?

Most people are conflicted when choosing to pay off debt or saving for emergencies.

You want to pay off debt, but not being prepared for emergencies can cause you to go further into debt.

So what’s the solution?

When paying off your debt, the first thing you should do is try and save up $1,000 for emergencies. $1,000 is enough money to pay for most minor emergencies and will allow you to use the majority of your money for debt repayment.

Simply pay the minimum balance on your other debts until you can save your first $1,000.

Debt Snowball

One of the most popular debt repayment strategies is the debt snowball, popularized by finance expert Dave Ramsey.

The debt snowball focuses on debt repayment based on paying off the smallest loan amount first regardless of interest rates. So for example, let’s say you have three loans:

- Car loan, $14,000 owed, 8% interest

- Credit card #1, $1,000 owed, 18% interest

- Credit card #2, $3,000 owed 7% interest

The debt snowball method would have you paying off Credit card #1 first, followed by Credit card #2, and finally your car loan.

While you work on paying off the first debt, you continue to make the minimum payments on the other debts.

The debt snowball is not the fastest method for debt repayment. The debt snowball is a motivation builder, because you’ll pay off your smallest debt quickly causing you to get excited about paying off your debt.

I recommend this debt strategy if you need motivation for paying off your debt. Otherwise, stick to the high-interest debt repayment strategy.

High-interest debt repayment

The high-interest debt repayment strategy is the least known strategy, but it happens to be the fastest way to pay off debt.

The strategy is to pay off your debts based on the highest interest rate, regardless of the amount owed. So looking at our three debts again:

- Car loan, $14,000 owed, 8% interest

- Credit card #1, $1,000 owed, 18% interest

- Credit card #2, $3,000 owed, 7% interest

The high-interest strategy would have you pay off Credit card #1, then your Car loan, and finally your Credit card #2.

While this is the fastest strategy to pay off your debt, it doesn’t do well for building motivation, which is the strength of the debt snowball.

I recommend this strategy if you don’t need motivation and want your debt paid off ASAP.

Quick tips to save money for debt repayment

You’ve created an awesome budget, evaluated your income, and decided on a debt repayment strategy. That’s awesome! But what’s next?

It’s time to start throwing as much money at your debts as possible and get aggressive about debt repayment!

There are a few short-term strategies that you can do to generate more cash to use on your debts. The keyword is “short-term” as most of these won’t be things you do for a lengthy period of time.

Sell your unused items

We tend to accumulate a bunch of useless junk over the years. It sits in our garage and takes up room in our sheds, unused for years.

We buy storage units to store furniture that we “might” want to use someday, but have paid more in storage fees than the furniture is worth 10 times over.

Your junk is cluttering your life and can be sold for money to pay off your debt or reach your first $1,000 emergency fund.

Selling your unused items is one of the fastest ways to generate extra cash.

Start eating frugally

We spend a lot of money on food. Eating is one of the top expenses Americans face on a daily basis and we are literally eating our savings away.

Take some time to learn to eat frugally. Create meal plans, buy what you need for the week and stick to your shopping list!

You should be able to feed your family for less than $500 per month.

Related:

Work overtime or find a part-time job

I hate working overtime because a full-time job already takes over our lives. However, working overtime is very effective for paying off debt and a huge part of how we paid off 40% of our mortgage in 2 years.

Working overtime is exhausting, but is super effective for generating extra cash. I recommend working overtime to jump start your debt repayment process.

However, working long hours can cause significant burnout, so be sure to listen to your body.

Donate blood or plasma

Some blood and plasma centers will pay you to donate your blood or plasma. You can do a quick google search to find these centers near you.

Debt repayment strategies to avoid

There are a few debt strategies that you should avoid at all costs. Here are a few examples of what you should avoid!

Loan consolidation

Loan consolidation doesn’t work. People who look at loan consolidation think it would be nice to have your debt all on one central loan.

The problem?

Your loan will take way longer to pay off! Keep your individual loans and you’ll pay off debt faster.

Home equity loans

Home equity loans borrow money against your house. It is never a good idea to borrow money against your house!

The problem?

If you fail to make your loan payments, you could lose your house. It’s a risky option that could cause you to lose your house and still owe money to your other debts.

401k loans

A 401k loan is where you’re borrowing money against your retirement fund.

The problem?

There are too many taxes and fees associated with doing so. Not to mention you’re hamstringing your retirement plan just to pay off debt.

A solid debt repayment plan will allow you to save for retirement and pay off debt.

If you’re wanting to pay off debt, build wealth, and become financially fit, take our free course on saving money and budgeting. The course is full of information to help your family and finances!

TightFist Finance

John is the founder of TightFist Finance and an expert in the field of personal finance. John has studied personal finance for over 10 years and has used his knowledge to pay down debt, grow his investment portfolio, and launch a financial based business. He is committed to sharing content related to personal finance based on his experience in his career, investing, and path towards reaching financial independence.