You don’t suck at budgeting. You just need a step by step process to make starting your budget easy.

I think we all know the importance of budgeting. Without budgeting, we can’t track our money and would most likely spend our money until it’s gone. Budgeting keeps us going in the right direction so we can meet our financial goals in life.

Today I’m giving you a simple step by step process to start your budgeting. It’s fairly straightforward and you could have your first budget drafted in less than an hour.

Don’t forget to take the free budgeting and save money course. The course goes into more detail about building an awesome budget and saving more money for your family.

This post may contain affiliate links which provide a commission and supports this blog. Thank you for your support!

How to start a budget when you suck at budgeting

Step #1 – Write down your income

Grab a notebook and write down how much money you earn each month, after tax. You will want to write down your base income, so don’t include any additional money earned from overtime.

Your written income should be the lowest pay expected. This is especially true if you’re paycheck varies from month to month. People who work a sales based jobs that pay a commission should write down their lowest expected earnings.

For example, if your monthly household income ranges anywhere from $2,500 to $3,500, write down $2,500.

Related:

- How to save a TON of money

- How to PAY OFF your home quickly! Our story of how we paid off 40% of our mortgage in 2 YEARS!

- Need a home down payment? Here’s how to save money for your house quickly!

Step #2 – Write down all your necessary expenses

You have certain expenses that you must pay every month in order to keep surviving. These include rent/mortgage, utility bills, groceries, fuel, cell phone bills, minimum debt payments, etc.

Write down the expense and the minimum amount owed each month.

The goal is to have all your expenses less than your smallest earned income. You wouldn’t want to build a budget on an income of $3,000 if your income ranges from $2,500 to $3,500.

If you did, you might have some good months and other bad months where you struggle to make ends meet. Instead, building a budget on your lowest earned income ensures that you are always prepared for your normal expenses. Any additional income over your lowest earned income usually goes towards savings or paying off debt.

Step #3 – Determine your grocery budget

The first thing you should do is determine how much money you have been spending on food each month. You can look through your old bank statements to get an idea.

Are you spending more than $500 per month on food?

Most families should be able to live comfortably on $500 per month on groceries. If you find yourself spending more than $500, try cutting back slowly to adjust down.

Related:

- What should you do if you’re BROKE and BARELY SURVIVING?

- How to recover from a BAD financial month.

- How to SAVE $20,000 in 2 YEARS!

Step #4 – Write down your other minor expenses

What are the other things do you regularly spend your money on?

Your minor expenses are all the non-necessities. Gym memberships, fun spending money, a hobby budget, etc.

Write down your minor expenses and about how much you plan to spend each month on each. Review the list again because it can be easy to forget something!

Step #5 – Check: Are your expenses greater than your income?

One of the biggest problems people have with their finances is spending more than they earn. Add up your monthly expenses and compare them to your income. Are you spending more money than you earn?

For example, you bring home $1,000 per month and only needed to budget for food, rent, and savings. Dedicating $800 to rent and $500 to food is going to generate $300 worth of debt each month!

It would be better to see something more like $700 for rent, $275 for food, and $25 for savings. See how your expenses and savings add up to your income? Every dollar earned is assigned a category.

Related:

What to do if your expenses are greater than your income

Start by reducing your spending in non-necessary expenses if your expenses are greater than your income. If needed, you may have to give up certain activities in order to make your finances work. Remember, you’ll want to have money left over at the end of each month to put into savings.

Have you reduced your expenses as far as possible, but are still struggling? Look for opportunities to swap providers. For example, you might save more money on your phone bill switching from AT&T to Ting.

Should all else fail, you’ll need to find a way to increase your income. You can get a part-time or full-time job, work more overtime, change jobs, look for freelance work, work from home, etc.

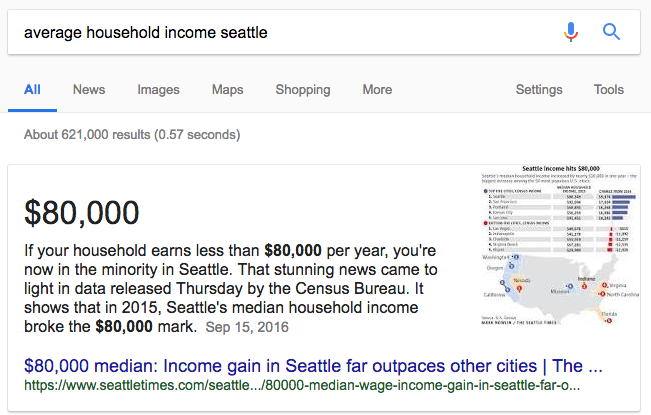

Is your income adequate?

One common problem people have with their finances is that they don’t earn enough money. You should check to see if you earn enough money for your area.

Start by googling your cities average household income. How does your income compare?

You should consider finding ways to increase your income if you find yourself average or below. The best thing you can do for your finances is start earning above average income. Earning more than most people around you will better your finances, allowing you to save more money.

Step #6 – Determine how much money can be saved

You should have a good idea of your monthly expenses and income. How much money is left over?

You would save $300 each month if you earned $1,000 per month and your expenses were $700. That $300 is the money you have to save or pay off more debt.

Where are you putting your savings? Some people keep their saved money into a savings account, others a money market. Investing your money is always a good option!

Are you happy with how much you’re saving? Do you want to save more money? If so, what can you do to increase how much money you’re saving?

Step #7 – Identify where you stand on Dave Ramsey’s 7 baby steps

Dave Ramsey is a famous personal finance guru. He developed seven baby steps to follow in order to turn your finances around, pay off debt, and build wealth.

Dave’s method has helped thousands of people get ahead in life. You can read the full article on the seven baby steps here. What step are you on now?

Baby Step #1 – $1,000 Emergency Fund

Baby Step #2 – Pay off all debt except your house

Baby Step #3 – 3 to 6 months of expenses saved for emergencies

Baby Step #4 – Invest 15% of income into pre-tax retirement

Baby Step #5 – Fund your children’s college education

Baby Step #6 – Pay off your home

Baby Step #7 – Build wealth and give generously

Knowing these steps will help keep you on track to financial freedom. Identify the step you’re currently working on and work towards reaching the next step.

Step #8 – Figure out your retirement plans

The sooner you can invest the better! Take advantage of any company matching and work towards investing 15% of your income into pre-tax retirement.

Personally, I invest in the program my work has set up. However, there are a lot of different options. Financial advisors are usually willing to sit down and discuss them with you.

Step #9 – Identify your savings goals

This is your money, what do you want to spend it on?

While I do advocate for you saving your money, but you’ll also want to buy things. Maybe a new couch or tools for the garage?

Most broke people go out and buy things when they want them. You’re smarter than that though. Smart people identify what they want, set a priority list, and then save money to buy.

Always buy cash in hand. The only exception is with something large, like your house.

Step #10 – Update your budget consistently

A budget is never set in stone. As a matter of fact, your budget will constantly be changing.

My wife and I sit down at the end of each month and discuss our budget. We look to see if we are struggling in certain categories or if we are saving too much. We then make adjustments as necessary.

You might need to increase your budget or change your habits if you overspend in a category such as food. Consider lowering your budget if you’ve got $5,000 saved up for “car tire replacement.”

You should also make budget entries regularly. If you’re new to budgeting then you should consider updating your budget daily. You can then try weekly once you’ve gotten into a habit of budgeting consistently.

If you’re wanting to build an awesome budget, take the free budgeting and save money course. The course is full of budgeting and save money tips that will help your family budget better and save more money.

TightFist Finance

John is the founder of TightFist Finance and an expert in the field of personal finance. John has studied personal finance for over 10 years and has used his knowledge to pay down debt, grow his investment portfolio, and launch a financial based business. He is committed to sharing content related to personal finance based on his experience in his career, investing, and path towards reaching financial independence.