Money management basics aren’t taught in school. You are taught how to be a good employee, but never about managing your life.

Besides, why would managing your life be important?

How would you like to be in complete control of your money? Your car breaks down and you’re not worried because you actually have the money to fix the problem.

Unfortunately, most people go through life where money manages them. People panic when the car breaks down because they don’t have the $500 required to fix it.

If you’re constantly worried about money, you’ve come to the right place. Today, I’m going to show you money management basics that will improve your financial situation. All you have to do is apply these principals to your life.

This article may contain affiliate links which pays a commission and supports this blog. Thank you for your support!

The basic process for money management

Unfortunately, some of us realize late in life that we have to manage our money. Imagine being 55 years old and waking up one day with this realization.

Absolutely zero money in your bank account and only ten years away from when you’re supposed to retire!

The first step in money management basics is self realization. One day we wake up and realize we have to manage our money before it manages us. Hopefully, this came early in your life, but it’s still manageable if you’ve come to this realization late in life.

Next, you need to take control of your finances. Starting a budget, controlling and reducing your expenses, and paying off debt are examples of taking control. Taking control of your finances isn’t easy, but it is well worth it.

Finally, the real magic begins when you start investing your money and finding ways to grow your income. Investing and increasing your income are where the real wealth building begins.

So where do we get started? Let’s take a look at the first money management basic, starting a budget.

Click to Tweet! Please Share!Click To TweetStart a budget

Starting a budget is the first step everyone needs to take when managing their money. Simply put, your budget is the plan you have for your money so you know how much money goes where.

You need a budget otherwise you’ll end up spending your money. A budget allows you to track your spending and identify problem areas. You would be surprised at how much money you spend on food if you actually tracked spending.

If you make $50,000 per year, you’ll end up making $500,000 over the course of 10 years. Do you really want to spend half a million dollars and have nothing to show for it?

Spending money is incredibly easy. Sticking to a budget requires discipline and teamwork for couples.

So how do you start a budget?

The first thing you want to do when starting a budget is determine your annual net income. From here, you should be able to determine how much money you have on a monthly basis.

Next, create a list of your expenses, bills, savings goals, and frequent purchases. What percentage of your monthly income should be allocated to each expense? How much money should you budget for groceries, rent, investing, etc?

Remember, every dollar you make should be budgeted.

Can you live off of your budget or are you living paycheck to paycheck? Are you saving enough for retirement?

Build an emergency fund

One of the money management basics that is often forgotten about is your emergency fund. An emergency fund is money you set aside for the sole purpose of an emergency, like a job loss.

Dave Ramsey recommends building a $1,000 emergency fund before you start paying off your remaining debt. Once you’re debt is paid off, it’s generally a good idea to keep 3 to 6 months expenses in a safe location.

Personally, I keep my emergency fund in a money market. A money market is a slightly higher interest bearing account that you can open up through your credit union. I have access to this money at a moments notice.

Click to Tweet! Please Share!Click To TweetPay off debt

Paying off debt is critical for effectively managing your money. Remember, the goal of money management is to invest as much money as possible so one day you can retire.

When you have a lot of debt it can be nearly impossible to get ahead. Add up all the car, credit card, student loans, and other debt you have. What would you do with that money if you weren’t paying off all that debt?

There are two common ways of paying off debt, the debt snowball method or paying off the highest interest rate first. The debt snowball is good for those who need motivation to pay off debt, but it’s a slower method. Paying off the highest interest rate is the quickest way to pay off your debt.

The debt snowball involves paying off your debts from smallest amount to largest, in that order. You pay the minimum all debts except for the one you’re trying to pay off first. You’ll get a few quick wins with this method which helps build motivation.

Paying off the highest interest rate first is the fastest method, paying off all your debt quickly.

Using credit cards responsibly

Credit cards are not bad. How we choose to use our credit cards is what can work to our favor or cause financial problems.

So how do you responsibly use credit cards? Only use a credit card for money you have and pay it off every month. It’s that simple, but it’s a challenging task for most.

Invest your money and plan for retirement

If you’ve finally gotten control over your money, then it’s time for you to grow wealth. Investing your money is the fastest way to retirement.

Your goal should be to lower your expenses and invest your extra money before you have a chance to spend it. So what does that look like exactly?

Ideally, your emergency fund is in a money market account. Set a maximum amount of money to keep in your checking or savings account. Anything over that maximum gets invested into your brokerage account.

For example, I maintain a $8,000 maximum in my checking account. Once I have more than $8,000 in my checking account, the difference is sent to my Vanguard account to be invested.

Finding a brokerage account

A brokerage account is the middle man between you and the stock market. If you want to invest your money, then you will need to open up an investment account with a brokerage firm.

There are many options, but I use Robinhood, TD Ameritrade, and Vanguard. You don’t need three accounts, but I have different brokerages for different reasons.

Robinhood is as basic as it gets. It is an easy to use platform where you can make trades with a few swipes in the app. If you’re just getting started in the stock market, Robinhood is a good start.

TD Ameritrade, specifically Think or Swim, is one of the best platforms for looking at stock charts. I love doing my stock research using the Think or Swim platform, but it’s a bit more advanced.

Vanguard is one of my favorite brokerage accounts because they offer a lot of low cost index funds for investing. Technically, you could invest in Vanguard funds through other brokerage accounts, but I still use Vanguard.

Click to Tweet! Please Share!Click To TweetWhat do I invest in?

There are a lot of different options for investing. Personally, I’m a huge fan of dividend stock investing, but you need to know what you’re doing if picking individual stocks.

For most individuals, investing in low cost Exchange Trade Funds (ETFs) are the way to go. Exchange Trade Funds are a collection of stocks that you can purchase for one low cost. Exchange Trade funds are a good and easy way to diversify your investments.

For example, VTI is the Vanguard Total Stock Market fund. VTI attempts to track the overall stock market and is currently trading for $123 per share. Purchasing one share of VTI means you own a portion of 3,521 stocks!

That’s a lot of diversification!

You can browse the entire list of Vanguard ETFs to start your search. Each ETF has it’s own investment goal, so be sure to understand what you’re investing in.

You should also consider your age and risk tolerance. Personally, I’m in favor of investing in all stocks, but I can handle market volatility. If you’re closer to retirement, you may consider a mixture of bonds and stocks to limit volatile market changes.

Are you investing solely for retirement? Vanguard offers target retirement date funds, which automatically add more bonds and conservatism as you approach your estimated retirement date.

Grow your income

The last step in money management basics is growing your income. Thus far, you’ve gained control of your money and started building wealth. Now, your job is to grow your income so you can invest more and build more wealth.

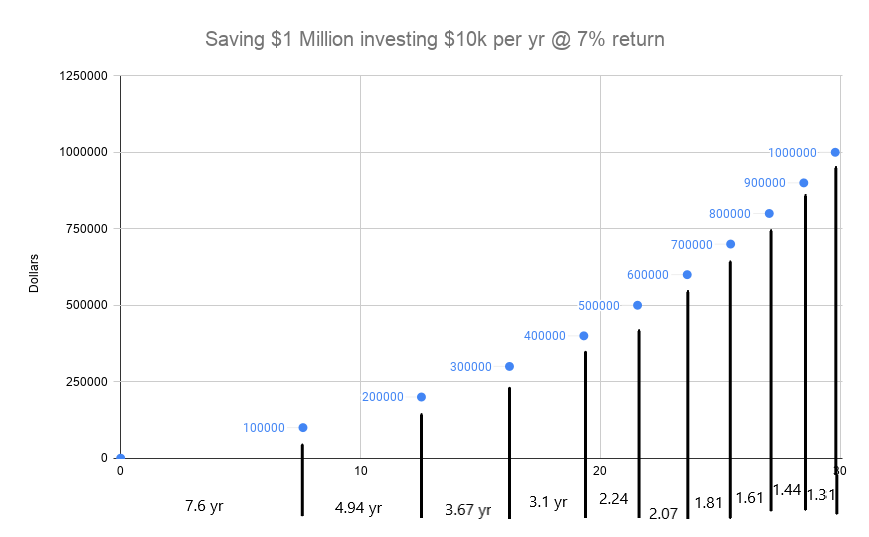

When you’re trying to save money for retirement, only two things matter. How much money you invest and your rate of return.

For most of us, investing in the stock market produces a return on investment around 10 percent annually. We have more control over our income and how much money we invest.

Imagine two people with the same expenses, say $40k per year. One person makes $50k and the other $70k. The first person is able to invest $10k per year, but the other person invests $30k per year. The second person can save more money because they have a higher income.

You can grow your income in a few different ways, career choices and side hustles. With career choices you can job hop, get performance pay increases, etc. Side hustles allow you to make money consistently and you’re paid according to your efforts.

Click to Tweet! Please Share!Click To TweetSummary: Personal money management basics

As you can see, there is a lot to know about money management. The first thing anyone needs to do is gain control of their money once they realize money management is a must.

Starting a budget is the first step to managing your money. You need a budget to track your income and ensure you’re meeting your money savings goals.

You’ll need to create an emergency fund to protect yourself from unfortunate life events. Your emergency fund should be a minimum of $1,000 to begin, but aim for 3-6 months expenses.

Aim to pay off your debt, keep debt away, and use credit cards responsibly. Debt hinders your ability to grow wealth. Finances is a game and the reward for great money management is retirement. Debt subtracts from your ability to retire early.

You need to create a plan to build wealth through investing. A brokerage account, like Robinhood or Vanguard, will allow you to invest your money. I recommend looking into low cost Exchange Trade Funds for investors.

Lastly, you need to grow your income and wisely invest the increases. Most people use their growing income to expand their lifestyle. However, the smart way to use your growing income is to add to your investments.

TightFist Finance

John is the founder of TightFist Finance and an expert in the field of personal finance. John has studied personal finance for over 10 years and has used his knowledge to pay down debt, grow his investment portfolio, and launch a financial based business. He is committed to sharing content related to personal finance based on his experience in his career, investing, and path towards reaching financial independence.